You can calculate trends in numeric data and predict

values beyond the range of those stored in the data source by using

the Forecast feature.

The calculations you can make to identify

trends and forecast values are:

xUsing a Simple Moving Average

A simple moving average is a series of arithmetic means

calculated with a specified number of values from a field. Each

new mean in the series is calculated by dropping the first value used

in the prior calculation, and adding the next data value to the

calculation.

Simple moving averages are sometimes used to analyze trends in

stock prices over time. In this scenario, the average is calculated

using a specified number of periods of stock prices. A disadvantage

to this indicator is that because it drops the oldest values from

the calculation as it moves on, it loses its memory over time. Also,

mean values are distorted by extreme highs and lows, since this

method gives equal weight to each point.

Predicted values beyond the range of the data values are calculated

using a moving average that treats the calculated trend values as

new data points.

The first complete moving average occurs at the nth data

point because the calculation requires n values. This is

called the lag. The moving average values for the lag rows are calculated

as follows: the first value in the moving average column is equal

to the first data value, the second value in the moving average

column is the average of the first two data values, and so on until

the nth row, at which point there are enough values to

calculate the moving average with the number of values specified.

x

Procedure: How to Calculate a Simple Moving Average

-

With

the By or Across field you want to use for your calculations, click Forecast.

The Forecast dialog box opens.

-

If you

want to change the name of the output field that displays the Forecasted

values, edit the default name that exists in the Field Name field.

-

Click Moving

Average from the Step 1: Choose a Method drop-down list.

-

Select

an input measure field from the Step 2: Choose a Measure drop-down

list.

If you select the same field as the By or Across field,

this field will not appear in the output even if it is included

in a display command.

-

Select

the increment number to count each instance of the By or Across

field from the Step 3: Choose The Interval menu.

-

Select

the number of predictions to be calculated for the Forecast field

from the Step 4: Choose Number of Predictions menu.

-

Select

the number of values to average from the Step 5: Choose Number Of

Values to Average menu.

-

Optionally,

change the default field format by clicking the Change

Format button and selecting a different format from

the Format dialog box.

-

Click OK.

x

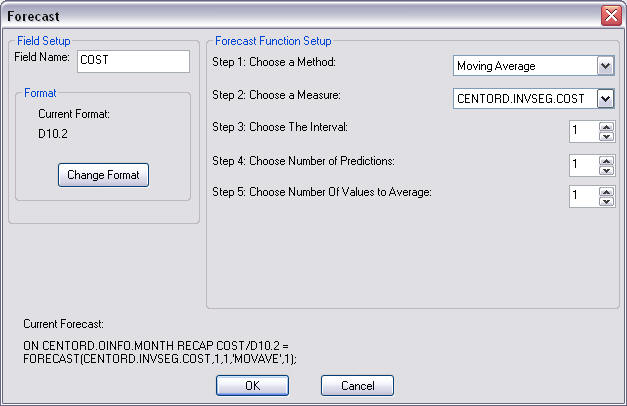

Reference: Forecast Dialog Box - Moving Average

The

Forecast dialog box is shown in the following image.

The

Forecast dialog box contains the following fields or options.

Field Setup

-

Field Name

- Is the Forecast field name.

-

Current Format

- Displays the format of the Forecast.

-

Change Format

- Opens the Format dialog box.

-

Forecast Function Setup

-

Step 1: Choose a Method

- Is the Forecast method to use to predict values. The options

are:

Double Exponential Average. Accounts for the tendency

of data to either increase or decrease over time without repeating.

Exponential Average. Calculates

a weighted average between the previously calculated value of the

average and the next data point.

Linear Regression. Derives

the coefficients of a straight line that best fits the data points

and uses this linear equation to estimate values.

Moving Average. Calculates

a series of arithmetic means using a specified number of values

from a field.

Multivariate Regression. Predicts two

or more dependent variables using one independent variable.

Triple Exponential Average. Accounts

for the tendency of data to repeat itself in intervals over time.

-

Step 2: Choose a Measure

- Is the field to be used to calculate the Forecast field.

-

Step 3: Choose The Interval

- Is the increment by which to count instances of the By or Across

field.

-

Step 4: Choose Number of Predictions

- Is the number of predictions to be calculated.

-

Step 5: Choose Number Of Values to Average

- Is the number of values to use to calculate the average used

to predict values.

-

Current Forecast

- Displays the code created by the Forecast dialog box.

Example: Calculating a Simple Moving Average

Create a new procedure, open with Report

Painter, and open the centord.mas file.

- Select Report at

the top of the Report Painter window, then select Define from

the drop-down list.

The Define dialog box opens.

- Enter PERIOD

in the Field input area, type I2 (Integer format) in the Format

input area, then double-click MONTH in the Fields List to add it

to the area below PERIOD, then click OK.

- Add the PERIOD, REGION, QUANTITY,

and LINE_COGS fields to the report.

- Select the PERIOD field

and click the By button.

- Select the QUANTITY field

and click the Sum button.

- Click the Where button

from the Where/If button.

The Expression Builder opens.

- Select REGION from

the Data section.

- Enter REGION

EQ 'WEST' Advanced section, and click OK.

- Click the Forecast button.

The

Forecast dialog box opens.

- In the Field

Name field, enter MOVING_AVE.

- Select Moving

Average from the Step 1: Choose a Method drop-down list.

- Select LINE_COGS from

the Step 2: Choose a Measure drop-down list.

- Specify 1 in

the Step 3: Choose The Interval menu.

- Specify 3 in

the Step 4: Choose Number of Predictions menu.

- Specify 3 in

the Step 5: Choose Number of Values to Average menu.

- Click OK.

- Run the report.

The

output is shown in the following image.

In

the report, the number of generated values to use for the moving

average is 3, and there are no REGION, QUANTITY, or LINE_COGS values

for the generated PERIOD and MOVING_AVE fields.

Each MOVING_AVE

field is computed by adding the three previous LINE_COGS values together

and dividing the total by three. When moving into the future, where

a LINE_COGS value is not available, the value of the last calculated

MOVING_AVE is substituted for the missing LINE_COGS value. The calculations

of the generated moving averages are explained here:

- The twelfth

MOVING_AVE value (3,579,303.67) is equal to the average of the LINE_COGS

values for PERIODs 10, 11, and 12. The calculation is (3,786,505.00

+ 4,427,791.00 + 2,523,615.00)/3.

- The thirteenth

MOVING AVE value (3,510,236.56) is equal to the average of the LINE_COGS

values for PERIODs 11, 12, and 13 (where the twelfth MOVING_AVE

value is substituted for the zero LINE_COGS value for PERIOD 13).

The calculation is (4,427,791.00 + 2,523,615.00 + 3,579,303.67)/3.

- The fourteenth

MOVING AVE value (3,204,385.07) is equal to the average of the LINE_COGS

values for PERIODs 12, 13, and 14 (where the twelfth and thirteenth MOVING_AVE

values are substituted for the zero LINE_COGS values for PERIODs

13 and 14). The calculation is (2,523,615.00 + 3,579,303.67 + 3,510,236.56)/3.

- The fifteenth

MOVING AVE value (3,431,308.43) is equal to the average of the LINE_COGS

values for PERIODs 13, 14, and 15 (where the thirteenth and fourteenth MOVING_AVE

values are substituted for the zero LINE_COGS values for PERIODs

14 and 15). The calculation is (3,579,303.67 + 3,510,236.56 + 3,204,385.07)/3.

xUsing Triple Exponential Smoothing

Triple exponential smoothing produces an exponential

moving average that takes into account the tendency of data to repeat

itself in intervals over time. For example, sales data that is growing

and in which 25% of sales always occur during December contains

both trend and seasonality. Triple exponential smoothing takes both

the trend and seasonality into account by using three equations

with three constants.

For triple exponential smoothing you,

need to know the number of data points in each time period (designated

as L in the following equations). To account for the seasonality,

a seasonal index is calculated. The data is divided by the prior

season index and then used in calculating the smoothed average.

- The first equation

accounts for the current time period, and is a weighted average

of the current data value divided by the seasonal factor and the

prior average adjusted for the trend for the previous period. The

weight constant is k:

SEASONAL(t) = k * (datavalue(t)/I(t-L)) + (1-k) * (SEASONAL(t-1) + b(t-1))

- The second equation

is the calculated trend value, and is a weighted average of the difference

between the current and previous average and the trend for the previous

time period. b(t) represents the average trend. The weight

constant is g:

b(t) = g * (SEASONAL(t)-SEASONAL(t-1)) + (1-g) * (b(t-1))

- The third equation

is the calculated seasonal index, and is a weighted average of the current

data value divided by the current average and the seasonal index

for the previous season. I(t) represents the average seasonal

coefficient. The weight constant is p:

I(t) = p * (datavalue(t)/SEASONAL(t)) + (1 - p) * I(t-L)

These equations are solved to derive the triple smoothed average.

The first smoothed average is set to the first data value. Initial

values for the seasonality factors are calculated based on the maximum

number of full periods of data in the data source, while the initial trend

is calculated based on two periods of data. These values are calculated

with the following steps:

- The initial trend

factor is calculated by the following formula:

b(0) = (1/L) ((y(L+1)-y(1))/L + (y(L+2)-y(2))/L + ... + (y(2L) -

y(L))/L )

- The calculation of

the initial seasonality factor is based on the average of the data values

within each period, A(j) (1<=j<=N):

A(j) = ( y((j-1)L+1) + y((j-1)L+2) + ... + y(jL) ) / L

- Then, the initial

periodicity factor is given by the following formula, where N is

the number of full periods available in the data, L is the number

of points per period and n is a point within the period (1<=

n <= L):

I(n) = ( y(n)/A(1) + y(L+n)/A(2) + ... + y((N-1)L+n)/A(N) ) / N

The three constants must be chosen carefully. The best results

are usually obtained by choosing the constants to minimize the mean-squared

error (MSE) between the data values and the calculated averages.

Varying the values of npoint1 and npoint2 affect the results, and

some values may produce a better approximation. To search for a

better approximation, you may want to find values that minimize

the MSE.

The equation used to forecast beyond

the last data point with triple exponential smoothing is:

forecast(t+m) = (SEASONAL(t) + m * b(t)) / I(t-L+MOD(m/L))

where:

- m

- Is the number of periods ahead for the forecast.

x

Procedure: How to Calculate a Triple Exponential Smoothing Average

-

With

the By or Across field you want to use for your calculations, click Forecast.

The Forecast dialog box opens.

-

If you

want to change the name of the output field that displays the Forecasted

values, edit the default name that exists in the Field Name field.

-

Click Triple

Exponential Average from the Step 1: Choose a Method

drop-down list.

-

Select

an input field from the Step 2: Choose a Measure drop-down list.

If you select the same field as the By or Across field,

this field will not appear even if it is included in a display command.

-

Select

the increment to count each instance of the By or Across field from

the Step 3: Choose The Interval menu.

-

Select

the number of predictions to be calculated for the Forecast field

from the Step 4: Choose Number of Predictions menu.

-

Select

the number of data points for a period from the Step 5: Choose The

Number of Points Per Period menu.

-

Select

the number of values to average from the Step 6: Choose Number Of

Values to Average menu.

-

Select

the number to use to calculate the weights for each term in the

trend from the Step 7: Choose The Number of Values For Each Trend

menu.

-

Select

the number to use to calculate the weights for each term in the

trend from the Step 8: Choose The Number of Values For Seasonal

Adjustment menu.

-

Optionally,

change the default field format by clicking the Change

Format button and selecting a different format from

the Format dialog box.

-

Click OK.

x

Reference: Forecast Dialog Box - Triple Exponential Average

The

Forecast dialog box is shown in the following image.

The

Forecast dialog box contains the following fields or options:

Field Setup

-

Field Name

- Is the Forecast field name.

-

Current Format

- Displays the Forecast format.

-

Change Format

- Opens the Format dialog box.

Forecast Functions Setup

-

Step 1: Choose a Method

- Is the Forecast method to use to predict

values. The options are:

Double Exponential Average. Accounts

for the tendency of data to either increase or decrease over time

without repeating.

Exponential Average. Calculates

a weighted average between the previously calculated value of the

average and the next data point.

Linear Regression. Derives

the coefficients of a straight line that best fits the data points

and uses this linear equation to estimate values.

Moving Average. Calculates

a series of arithmetic means using a specified number of values

from a field.

Multivariate Regression. Predicts two

or more dependent variables using one independent variable.

Triple Exponential Average. Accounts

for the tendency of data to repeat itself in intervals over time.

-

Step 2: Choose a Measure

- Is the field to be used to calculate the Forecast field.

-

Step 3: Choose The Interval

- Is the increment by which to count instances of the By or Across

field.

-

Step 4: Choose Number of Predictions

- Is the number of predictions to be calculated.

-

Step 5: Choose The Number of Points Per Period

- Is the number of data points in a period.

-

Step 6: Choose Number Of Values to Average

- Is the number of values to use to calculate the average used

to predict values.

-

Step 7: Choose The Number of Values For Each Trend

- Is the number used to calculate the weights for each term in

the trend. This value is available only for Double Exponential Average

and Triple Exponential Average.

-

Step 8: Choose The Number of Values For Seasonal Adjustment

- Is the number used to calculate the weights for each term in

the seasonal adjustment.

-

Current Forecast

- Displays the code created by the Forecast dialog box.

Example: Calculating a Triple Exponential Smoothing Average

Create

a new procedure, open with Report Painter, and open the centord.mas

file.

- Click Report at

the top of the Report Painter window, then click Define from

the drop-down list.

The Define dialog box opens.

- Enter PERIOD in

the Field input area, type I2 (Integer format)

in the Format input area, then double-click MONTH in

the Fields List to add it to the area below PERIOD, then click OK.

- Add the PERIOD, REGION, QUANTITY,

and LINE_COGS fields to the report.

- Select the PERIOD field

and click the By button.

- Select the QUANTITY field

and click the Sum button.

- Click the Where button

from the Where/If drop-down menu.

The Expression Builder opens.

- Select REGION from

the Data section.

- Enter REGION

EQ 'WEST' in the Advanced section, and click OK.

- Click the Forecast button.

The

Forecast dialog box opens.

- In the Field

Name field, enter TRPL_EXP_AVE.

- Click Triple

Exponential Average from the Step 1: Choose a Method

drop-down list.

- Select LINE_COGS from

the Step 2: Choose a Measure drop-down list.

- Specify 1 in

the Step 3: Choose The Interval menu.

- Specify 3 in

the Step 4: Choose Number of Predictions menu.

- Specify 3 in

the Step 5: Choose The Number of Points Per Period menu.

- Specify 3 in

the Step 6: Choose Number Of Values to Average menu.

- Specify 3 in

the Step 7: Choose The Number of Values for Each Trend menu.

- Specify 3 in

the Step 8: Choose The Number of Values for Seasonal Adjustment

menu.

- Click OK.

- Run the report.

When

the report is run, the forecasted triple exponential values will

appear in the TRPL_EXP_AVE column.

The output is shown in

the following image.

In

the report, the number of values used for each triple exponential

average is 3, and there are no REGION, QUANTITY, or LINE_COGS values

for the generated PERIOD and TRPL_EXP_AVE fields.

x

Forecast Reporting Techniques

You can use Forecast multiple times in one request.

However, all Forecast requests must specify the

same sort field, interval, and number of predictions. The only things

that can change are the Recap field, method, field used to

calculate the Forecast values, and number of points

to average. If you change any of the other parameters, the new parameters

are ignored.

If you want to move a Forecast column in the report output,

use an empty Compute expression for the Forecast field

as a placeholder. The data type (I, F, P, D) must be the same in

the Compute expression and the Recap expression.

To make the report output easier to interpret, you can create

a field that indicates whether the Forecast value in each row is a predicted

value. To do this, define a virtual field whose value is a constant

other than zero. Rows in the report output that represent actual

records in the data source will appear with this constant. Rows

that represent predicted values will display zero. You can also

propagate this field to a HOLD file.

Example: Generating Multiple Forecast Columns in a Request

This example calculates moving averages

and exponential averages for both the DOLLARS and BUDDOLLARS fields

in the GGSALES data source. The sort field, interval, and number of

predictions are the same for all of the calculations.

DEFINE FILE GGSALES

SDATE/YYM = DATE;

SYEAR/Y = SDATE;

SMONTH/M = SDATE;

PERIOD/I2 = SMONTH;

END

TABLE FILE GGSALES

SUM DOLLARS AS 'DOLLARS' BUDDOLLARS AS 'BUDGET'

BY CATEGORY NOPRINT BY PERIOD AS 'PER'

WHERE SYEAR EQ 97 AND CATEGORY EQ 'Coffee'

ON PERIOD RECAP DOLMOVAVE/D10.1= FORECAST(DOLLARS,1,0,'MOVAVE',3);

ON PERIOD RECAP DOLEXPAVE/D10.1= FORECAST(DOLLARS,1,0,'EXPAVE',4);

ON PERIOD RECAP BUDMOVAVE/D10.1 = FORECAST(BUDDOLLARS,1,0,'MOVAVE',3);

ON PERIOD RECAP BUDEXPAVE/D10.1 = FORECAST(BUDDOLLARS,1,0,'EXPAVE',4);

END

The output is shown in

the following image.

PER DOLLARS BUDGET DOLMOVAVE DOLEXPAVE BUDMOVAVE BUDEXPAVE 1 801123 801375 801,123.0 801,123.0 801,375.0 801,375.0

2 682340 725117 741,731.5 753,609.8 763,246.0 770,871.8

3 765078 810367 749,513.7 758,197.1 778,953.0 786,669.9

4 691274 717688 712,897.3 731,427.8 751,057.3 759,077.1

5 720444 739999 725,598.7 727,034.3 756,018.0 751,445.9

6 742457 742586 718,058.3 733,203.4 733,424.3 747,901.9

7 747253 773136 736,718.0 738,823.2 751,907.0 757,995.6

8 655896 685170 715,202.0 705,652.3 733,630.7 728,865.3

9 730317 753760 711,155.3 715,518.2 737,355.3 738,823.2

10 724412 709397 703,541.7 719,075.7 716,109.0 727,052.7

11 620264 630452 691,664.3 679,551.0 697,869.7 688,412.4

12 762328 718837 702,334.7 712,661.8 686,228.7 700,582.3

Example: Moving the FORECAST Column

The following example places the DOLLARS

field after the MOVAVE field by using an empty COMPUTE command as

a placeholder for the MOVAVE field. Both the COMPUTE command and

the RECAP command specify formats for MOVAVE (of the same data type),

but the format of the RECAP command takes precedence.

DEFINE FILE GGSALES

SDATE/YYM = DATE;

SYEAR/Y = SDATE;

SMONTH/M = SDATE;

PERIOD/I2 = SMONTH;

END

TABLE FILE GGSALES

SUM UNITS

COMPUTE MOVAVE/D10.2 = ;

DOLLARS

BY CATEGORY BY PERIOD

WHERE SYEAR EQ 97 AND CATEGORY EQ 'Coffee'

ON PERIOD RECAP MOVAVE/D10.1= FORECAST(DOLLARS,1,3,'MOVAVE',3);

END

The output is shown in

the following image.

Category PERIOD Unit

Sales MOVAVE Dollar

SalesCoffee 1 61666 801,123.0 801123

2 54870 741,731.5 682340

3 61608 749,513.7 765078

4 57050 712,897.3 691274

5 59229 725,598.7 720444

6 58466 718,058.3 742457

7 60771 736,718.0 747253

8 54633 715,202.0 655896

9 57829 711,155.3 730317

10 57012 703,541.7 724412

11 51110 691,664.3 620264

12 58981 702,334.7 762328

13 0 694,975.6 0

14 0 719,879.4 0

15 0 705,729.9 0

Example: Distinguishing Data Rows From Predicted Rows

In the following example, the DATA_ROW

virtual field has the value 1 for each row in the data source. It

has the value zero for the predicted rows. The PREDICT field is

calculated as YES for predicted rows, and NO for rows containing

data.

DEFINE FILE CAR

DATA_ROW/I1 = 1;

END

TABLE FILE CAR

PRINT DATA_ROW

COMPUTE PREDICT/A3 = IF DATA_ROW EQ 1 THEN 'NO' ELSE 'YES' ;

MPG

BY DEALER_COST

WHERE MPG GE 20

ON DEALER_COST RECAP FORMPG/D12.2=FORECAST(MPG,1000,3,'REGRESS');

ON DEALER_COST RECAP MPG =FORECAST(MPG,1000,3,'REGRESS');

END

The output is:

DEALER_COST DATA_ROW PREDICT MPG FORMPG

2,886 1 NO 27.00 25.65

4,292 1 NO 25.00 23.91

4,631 1 NO 21.00 23.49

4,915 1 NO 21.00 23.14

5,063 1 NO 23.00 22.95

5,660 1 NO 21.00 22.21

1 NO 21.00 22.21

5,800 1 NO 24.20 22.04

6,000 1 NO 24.20 21.79

7,000 0 YES 20.56 20.56

8,000 0 YES 19.32 19.32

9,000 0 YES 18.08 18.08